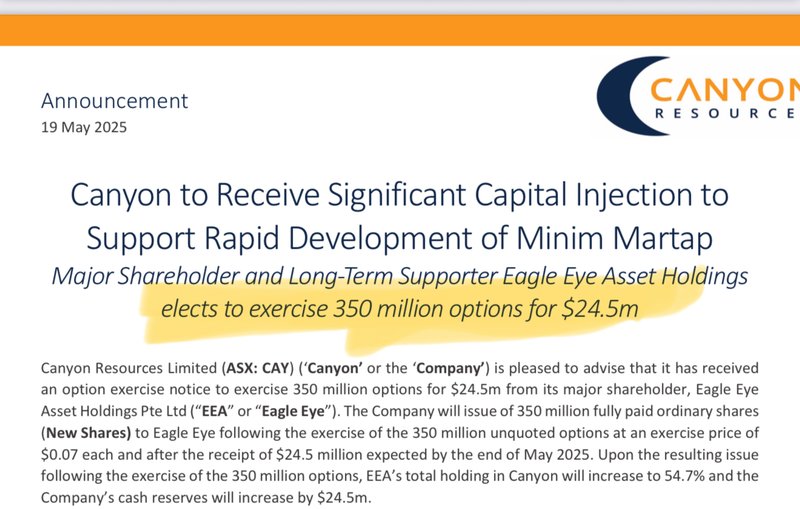

CAY banks $24.5M cash - Feasibility study due next quarter

Our bauxite Investment Canyon Resources (ASX: CAY) just added a big chunk of cash to its balance sheet.

CAY’s biggest shareholder Eagle Eye Asset Management just exercised $24.5M in 7c options.

Means CAY should now have more than $30M cash in the bank…

It also means Eagle Eye now hold 54.7% of CAY.

This cash injection is in addition to the US$123M debt underwriting Eagle Eye has committed to so that CAY can purchase all of its rail fleet.

Considering CAY’s last feasibility study had total CAPEX estimated at US$253M we think CAY is going into the project financing stage with a huge leg up from a cash perspective.

Almost half of the CAPEX is committed to (with that debt underwriting) and CAY has over $30M in cash in the bank.

AND there is another $10.5M CAY could end up getting if Eagle Eye exercises all of their remaining options.

We think CAY is now in a very strong position from a balance sheet perspective only a few months away from a Final Investment Decision (FID) on its project.

Next for CAY is its updated Definitive Feasibility Study (DFS) which is the precursor for CAY going into development.

That DFS is due in Q3 this year.

What we are hoping to see from the DFS:

CAY’s updated Definitive Feasibility Study is now due next quarter.

We think the study is an important catalyst because it will give the market a fresh perspective on the economics of CAY’s project.

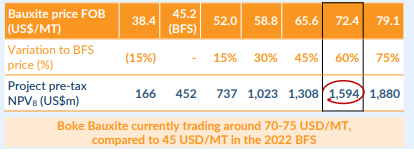

The previous study done in 2022 was done using a US$45.20/tonne bauxite price and returned a pre-tax Net Present Value (NPV) for the project of ~US$452M.

Bauxite prices are now above US$90/tonne…

A slide from CAY’s recent investor presentation gave us a pretty good idea of what to expect - with today’s spot prices more than quadrupling the project's NPV (to US$1.6BN) relative to the 2022 study:

(Source)

The NPV upgrade will ultimately dictate how the market values CAY.

Usually, as a project is getting closer to first production, its market cap will start to close the gap to its project’s NPV.

Before first production it’s not uncommon to see a stock trading at 40% to 80% of its project’s NPV.

For some context, just 40% of a US$1.6BN NPV would imply CAY should be capped at A$1BN+.

With first production now expected within the next 12 months, that means we could see that convergence start to happen in the short-medium term.

This is central to our CAY Big Bet which is as follows:

Our CAY Big Bet:

“CAY takes its bauxite project into production is re-rated to a market cap greater than $1BN”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our CAY Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

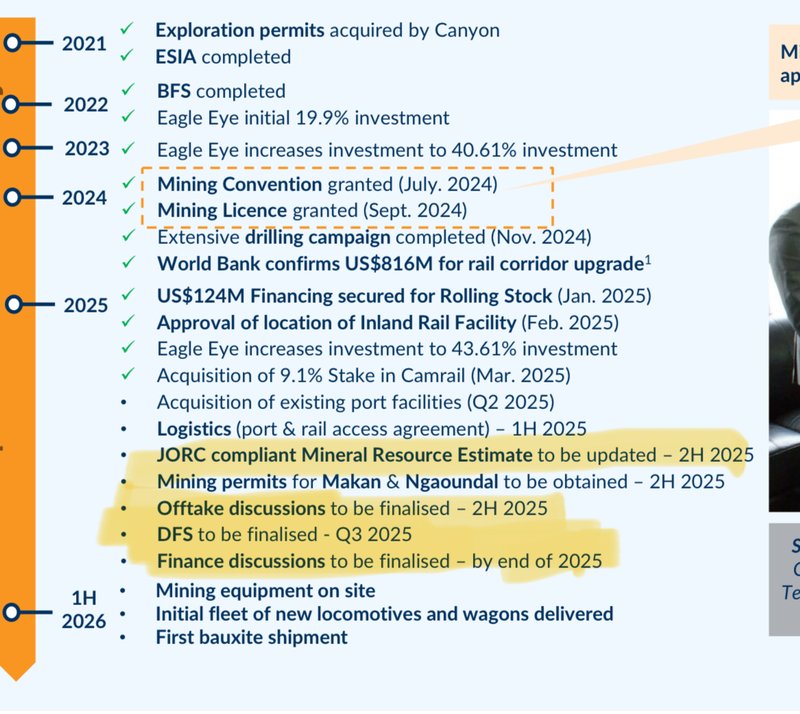

What’s next for CAY?

The slide below from CAY’s recent investor presentation gives a pretty good overview of what we can expect to see next:

(Source)

In the short term we are looking forward to an upgraded JORC resource, feasibility study results and some offtake news.